So, the land was re-staked [8/2/13]! And then it rained. And rained. And rained some more. Basically it rained about 10 days in a row. During a drought. We basically had no moisture for an entire year and it decided to rain the week we were going to break ground. However, I will say I am happy for the corn. The corn is happy and tall and green. I will also say that our grass on the land looks beautiful. Not something you usually see in August.

Author Archives: wnm9999

let’s build a house!

OR NOT. So, we closed on the construction loan in early May and expected to break ground in late May/early June. However, as always with this house, that did not happen.

We were asked to mow the area where the perk test would be done (for the septic system), so that the sun could reach the ground more easily and give us a better perk result. We were under a short time frame because were were leaving for vacation and would be gone 12 days. We expected that the perk test would be completed by the time we were back (May 29th). Wrong.

We were in the airport on the way back from our trip and I received a call from the builder saying that the perk test had not been done yet (What??? It had been 3 weeks since we closed on the loan!). Apparently it had rained a lot while we were gone and they were worried that it would not perk well if they proceeded.

So… we waited, and waited. Finally, towards the middle of June, the perk test was completed and we achieved a perk that did not necessitate an engineered septic system (yay!). However, at this point, interest rates had gone from 3.5% to 4.5% (WTF!). So, we were definitely stressed and just wanted to the process to move forward.

* Just a side note- a jump of 1% in interest rates causes our mortgage to go up $200/month.

Then, there was a little issue between the excavator and builder and the report did not get handed over that the builder needed for the building permit. We also had to wait for the surveyor to stake the land.

Towards the beginning of July, the builder finally had what he needed and proceeded to apply for the building permit. But wait! Nothing can be easy! The county advised the builder that we could not put our house on the land where we had staked it. Apparently, the 3 acres was “platted” and the 13 acres was not platted (basically zoned differently) and the house could not overlap onto the 2 pieces of land. We had no idea about this when we bought the land and although it is fixable, it would take another 45-90 days to re-zone the 2 pieces together (words were thrown around like “vacate” and I have no idea what that all means).

The county told the builder that we could put the house on the 3 acres or 13 acres. We were not interested in putting it on the 13 acres because it would be behind our neighbors house. If we put the house on the 3 acres though, we would need a new driveway because the current driveway was on the 13 acres (seriously?). Since that was the fastest route, we decided it was worth the approx. $2000 to put in a new driveway. Luckily, the perk test was done on the 3 acres so we didn’t have to re-do that. However, it did need re-staked and the surveyor had a 3 week wait. We also had to get an “entrance permit” that had to be approved by our township.

But wait! It has to be as hard as possible! When the builder took the new survey to the county they said, “well, they can’t have 2 driveways because that would be 2 tracts of land and the bank won’t like that”. Um what? So I can’t put it where I want it and I can’t put it where you said I should? I called the bank and they said it was no issue for them (like I said, best bank ever!). It eventually got wrapped up and we only had to wait for the surveyor to do his re-staking.

Patience is a virtue? What doesn’t kill you makes you stronger? — My mantras during July

construction loan

The construction loan was another hiccup in the building process for us. The first step is getting an appraisal. Our first bank (bank who we had the land loan with), would loan 80% of the appraised value. We started the appraisal process in February 2013. By the end of March, I still had not received the appraisal. After a lot of pushing, the loan officer sent it and much to my surprise, it was VERY low. Like, “we aren’t going to be able to build this house” low. It basically didn’t give us any credit for the steel building, and in turn did not leave us with much equity. We would have had to save an additional $20k in addition to our already large planned down payment amount.

So, I started calling banks. I happened to call a bank in town that was just awesome from the very first phone call. They said that they loan 85% of the value, which I knew would help us get closer to the amount we needed, even without a higher appraisal.

We met with the new bank and they agreed that the first appraisal was very low for the land worth, building and house. They submitted a new appraisal and it came back $20k higher than the first. That combined with loaning an extra 5% put us exactly where we needed to be. We were finally going to build the house!

Appraisal Summary:

– Appraises 85% of value (land+building+house plans)

– Uses comparables to other properties in the area

– Calculation (numbers used as examples):

* Appraised value= $100k

* 85%= $85k (amount they will loan)

* Cost to build house: $70k

* Amount owed on land: $25k

_______________________________________________

= $10k down payment

For our construction loan, our down payment does not need to be paid until the end of construction. Basically, once the builder has drawn all of the money in the construction loan, we will start paying the builder.

We are charged interest monthly based on the money that has been drawn from the account.

The construction loan is for 9 months, but we expect to be finished well before that (even with delays that we have experienced)

I cannot say enough about how great bank #2 was. If you are in my area and looking for a great bank, I would happy to give you the name.

becoming landlords

Well, I never thought we would be the type to own “investment properties”, but here we are. We listed our house in July 2012, and by October we had only one showing. Going into winter, we knew that the traffic would not pick up. We had another realtor come look at the house and he told us that there were many people in our same situation, and that many had decided to rent their houses out. Because interest rates were so low, we decided to re-finance our mortgage and keep our house as a rental (we are living with family during the building process). We were able to lock in a rate of 3.375%, which was exactly half of our initial rate (6.75%) when we bought the house July 2007.

Looking back at the re-finance process, I can only laugh. We were supposed to close on 12/24 and that didn’t happen. Then we were going to close on 12/26 and the mobile notary didn’t show up. Then we were actually on our way to meet the notary and they called and changed the time. And then they did it again. I seriously thought I was being “Punk’d”. Good grief. Good news was that I got my loan application fee back because of all the ridiculousness ($350). So, all’s well that ends well.

Our tenants moved in on December 1st and it has been pretty smooth so far. We had a few issues with the rental management company we hired to manage the property, but it is worth it in order to move forward with the building process.

bid process

We initially had a friend bid out the plans for us in March 2012, but when the bid came back in May, it was way too high. At that point, we were unsure if we were going to be able to build or not. I knew that houses were being built in our budget, so we decided to get bids from other builders in the area. We started this process in June and by August we had selected our builder. His bid was about $70k lower than our initial bid (I told you it was high!). We were very relieved, however we still had one last thing to accomplish before we could start- selling our house.

steel building

[completed October 2011] My husband was interested in putting up a steel building prior to building our house so that we would have storage for our belongings during the transition. We chose to work with a company that builds “Lester” steel buildings and chose a 40×40 style. The building has 14′ roof pitch, is insulated and has 6″ thick concrete floors in case he wants to use a car lift in the future. We also chose to put a small window in the ceiling so that we could use natural light until it is wired for electric. We chose white with grey trim to match the future built house.

house plan

[started June 2011, finished January 2012] the house plan/bid has been the longest and most frustrating part of the process. Fortunately, at this point we have completed that stage, but I will give a little explanation for the process we went through.

After we purchased the land, we casually searched the internet for house plans that we liked. The most important part was finding an exterior that we liked, because the interior could be rearranged to what we wanted. We came across an exterior that we both liked and an interior that could be changed minimally to what we wanted. The requirements were:

- ranch style

- potential for bonus room above garage [we ended up taking this out of the final plans. we decided to finish the basement instead]

- at least 3 bedrooms on the main level

- master bedroom with bathroom and 2 walk in closets

- half bath for guests off of living area

- full bathroom for 2 bedrooms

- master bedroom separated from other 2 bedrooms

- mudroom

- walk in pantry

- open floor plan

- fireplace

- 3 car garage

The plan i found [familyhomeplans.com]:

My drawing for the interior:

*I also had a plan for the basement as well, the final image is very similar

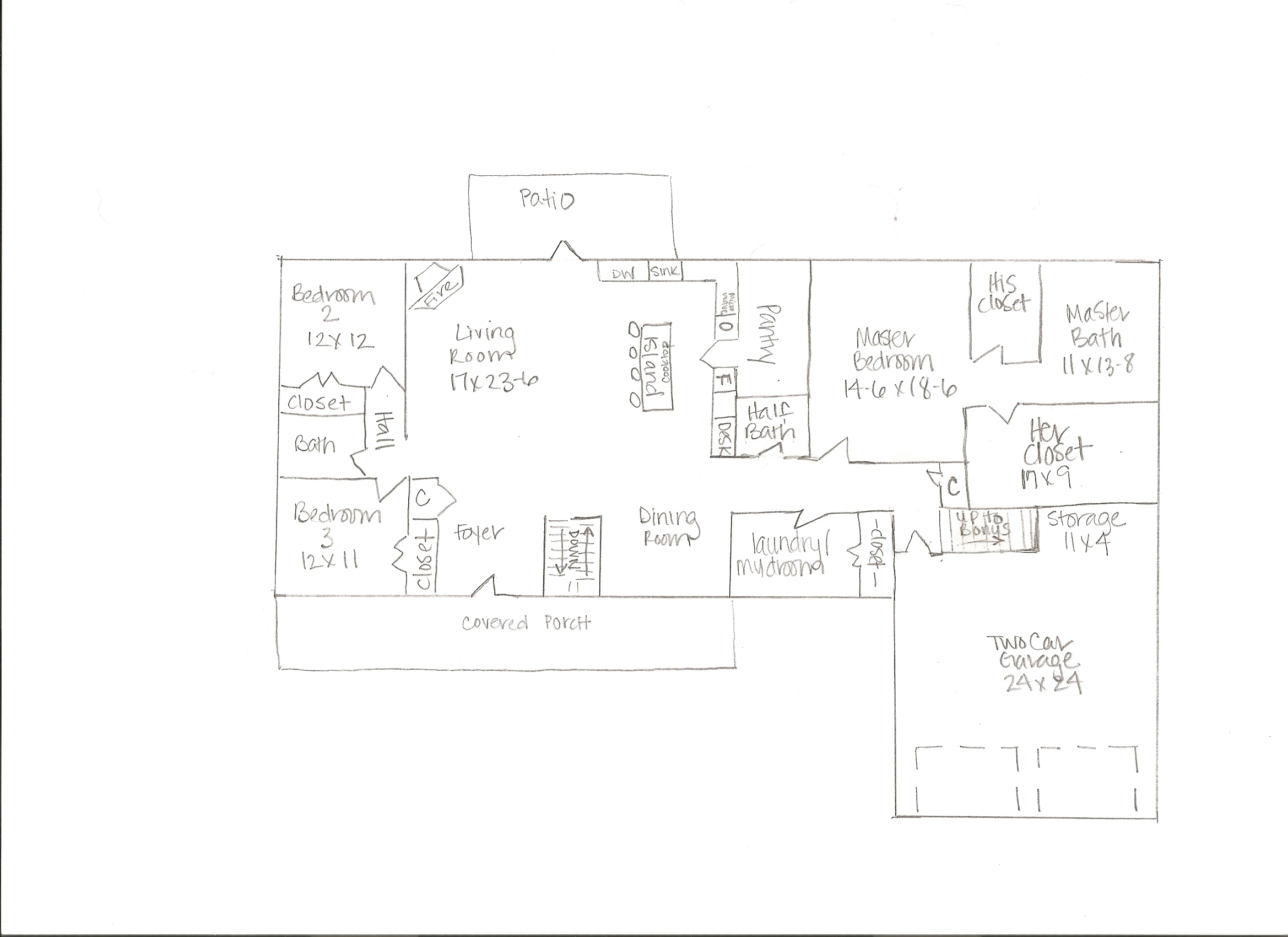

The final plan (after several iterations):

[we plan on having the exterior be white as the inspiration image]

[main floor]

[basement]

So I said it was a difficult process, right? Well, we met with the architect that worked for one of the local lumber companies. we gave him all of the details and within about 2 weeks we met with him to go over the initial plans. Everything was pretty good, but there were a few things to change. However, about a week or so later we found out that the lumber company went out of business. just closed their doors. So.. how were we going to get in contact with the architect? After a few weeks, he called us and he told us that he was going to continue to work on house plans from his home. Months went by and because we were not building soon, we were not a priority. Finally, in December, we received the revisions. We had a few small changes and in January they were complete. This was the start of another round of discouraging events…

our land

[july 2010] The first step in the process was buying our land. We had always talked about building, but did not have any concrete plans or a timeline for building. I would periodically look online at land listings and one day I found a list for 13 acres in the part of town we wanted and on blacktop. Our biggest requirements for the area we wanted was school district and no gravel. The price was great, so we went out to drive by the property. It just so happened that the realtor was mowing around the for sale sign, so we stopped to ask him about it. We found out that the owners were selling 25 acres total and the 13 acres we were interested in only had only 60 feet of frontage (grandfathered in). The majority of the property sat behind another house. This was not ideal and we realized that if we bought the 3 acres next the 13, it would solve the issue. Of course the 3 acre price was almost as much as the 13 acres, so we had to consider if the total cost for the 16 acres was worth it. We decided that it would be hard to find 16 acres anywhere, especially that met our requirements, for that price. We submitted an offer and the sellers countered back and we accepted. This by far was the most smooth part of our entire process so far.

Although the interaction with the realtor and making an offer is very similar to buying a house, the loan part is much different. Not many banks offer land loans and the terms are different. Local banks and credit unions are a good place to start. Our loan was for 20 years, 5 year ARM, which was not a big deal since we were hoping to start building before the 5 years was up. 20% is required as a down payment, so this is also where it differs from a conventional mortgage. The down payment becomes part of your equity when you go to obtain the construction loan (as long as the land does not depreciate).

We purchased the land for $14k under the appraisal, so this helped give us additional equity when we obtained our construction loan.

dogs at the land

welcome

I’m creating this blog to keep track of the building process and keep my plans for the new house organized. The name of the blog comes from a favorite song of mine that came out around the time we were buying our land and working on our house plans

Miranda Lambert’s “The House That Built Me”

{my favorite part}

“Mama cut out pictures of houses for years.

From ‘Better Homes and Garden’ magazines.

Plans were drawn, concrete poured,

and nail by nail and board by board

Daddy gave life to mama’s dream.”

Welcome!